Building Better Communities: Workforce Housing That Works for Everyone

Good housing changes lives. When teachers, firefighters, and healthcare workers can afford homes in the communities they serve, everyone benefits. We guide you to grants and financing that turn this vision into reality.

The Impact We Create Together

Economic Security

Homeownership builds generational wealth. Families gain equity instead of just paying rent.

Environmental Benefits

Rain gardens, energy efficiency, and lower utility costs help families and the planet.

Food Security

Local gardens reduce grocery bills and improve diet quality.

Community Resilience

Places where essential workers live and neighbors look out for one another.

How This Guide Helps You

Custom fits. The grants and timelines below are examples, not rules – your plan is tailored to local needs.

We handle complexity. Our team covers grants, financing, and community engagement so you focus on vision.

More options. Many other grants may suit your project; we'll surface them as needed.

Good news: Workforce housing is achievable with a clear roadmap. Think of it as four practical phases.

The Simple 4-Phase Approach

Phase 1

Plan & Prepare

$5K–$10K

Phase 2

Build Infrastructure

$500K–$4M

Phase 3

Construct & Market

$1M–$3M

Phase 4

Scale & Expand

$20M+

Start Here: Phase 1 Planning ($5K–$10K)

Seed money covers site analysis and community engagement – no need for millions upfront.

- Alabama Power Elevate: Up to $5K; next deadline 01 Nov 2025

- Regions Foundation: Invitation only; rolling

- Typical tasks: Feasibility studies, zoning checks, community meetings

▶ Full Phase Details

Phase 2 – Infrastructure & Remediation ($500K–$4M)

- EPA Brownfields Assessment: $0.5–4M (expected Nov 2025)

- Clean Water Fund Green Infrastructure: Rolling via Alabama program

- USDA Community Facilities: Rolling; amounts vary

Phase 3 – Construction & Market ($1M–$3M)

- FHLB Atlanta Affordable Housing Program: Up to $1.25M

- Alabama Housing Trust Fund: Rolling

Phase 4 – Operations & Expansion ($20M+)

- HUD Choice Neighborhoods: Up to $50M

- Enterprise / Wells Fargo Breakthrough: Innovation awards

Continuous Financing Alignment

Parallel financing preparation ensures you are ready when grant funds arrive:

- Set up single-family mortgage revenue bonds in Phases 2-3

- Leverage church/non-profit bond capacity while keeping ownership

- Build lender networks with Fannie Mae / Freddie Mac

- Coordinate with local housing authorities for bond issuance

- Avoid complex tax-credit compliance traps

Key Implementation Notes

- Grants can overlap within the same phase

- Several programs accept applications year-round

- Major federal programs need 6–12 months of prep time

- Early partnerships with banks and municipalities are essential

Grant Opportunities & Application Requirements

| Grant Program | Award Amount | Application Deadline | Eligible Applicants | Phase |

|---|---|---|---|---|

| Alabama Power Elevate | Up to $5K | 1 Nov 2025 | Nonprofit, Public | Phase 1 |

| Regions Foundation | By invitation; amounts vary | Rolling applications | Nonprofit, Public | Phase 1 |

| Environmental Protection Agency Brownfields Assessment | $0.5M - $4M | Request for Applications expected Aug 2025; apps due Nov 2025 | Nonprofit, Public (lead required) | Phase 2 |

| Clean Water State Revolving Fund Green Infrastructure (Alabama) | Varies by project; forgiveness terms available | Rolling through Alabama Department of Environmental Management | Public, Nonprofit w/municipal partner | Phase 2 |

| Department of Agriculture Community Facilities | Varies by rural area needs | Rolling applications | Public, Nonprofit | Phase 2 |

| Federal Home Loan Bank Atlanta Affordable Housing Program | Up to $1.25M | 2025 awards announced Oct 2025 | All types w/Federal Home Loan Bank member | Phase 3 |

| National Housing Trust Fund (Alabama) | ~$3M total state allocation | Rolling cycle through Alabama Housing Finance Authority | Nonprofit, Public | Phase 3 |

| Housing and Urban Development Choice Neighborhoods Implementation | Up to $50M | Notice of Funding Opportunity forecasted Q1 2026 (date TBD) | Public (lead required) | Phase 4 |

| Enterprise/Wells Fargo Breakthrough | $2-3M awards from $20M pool | Next round expected 2025-26 (date TBA) | All types (innovation focus) | Phase 4 |

Single-Family Homeownership Finance Models

This section outlines bond-based models for building and selling homes affordably—whether led by developers, churches, or nonprofit organizations. These approaches avoid tax credits and allow immediate sale, with no ongoing encumbrances.

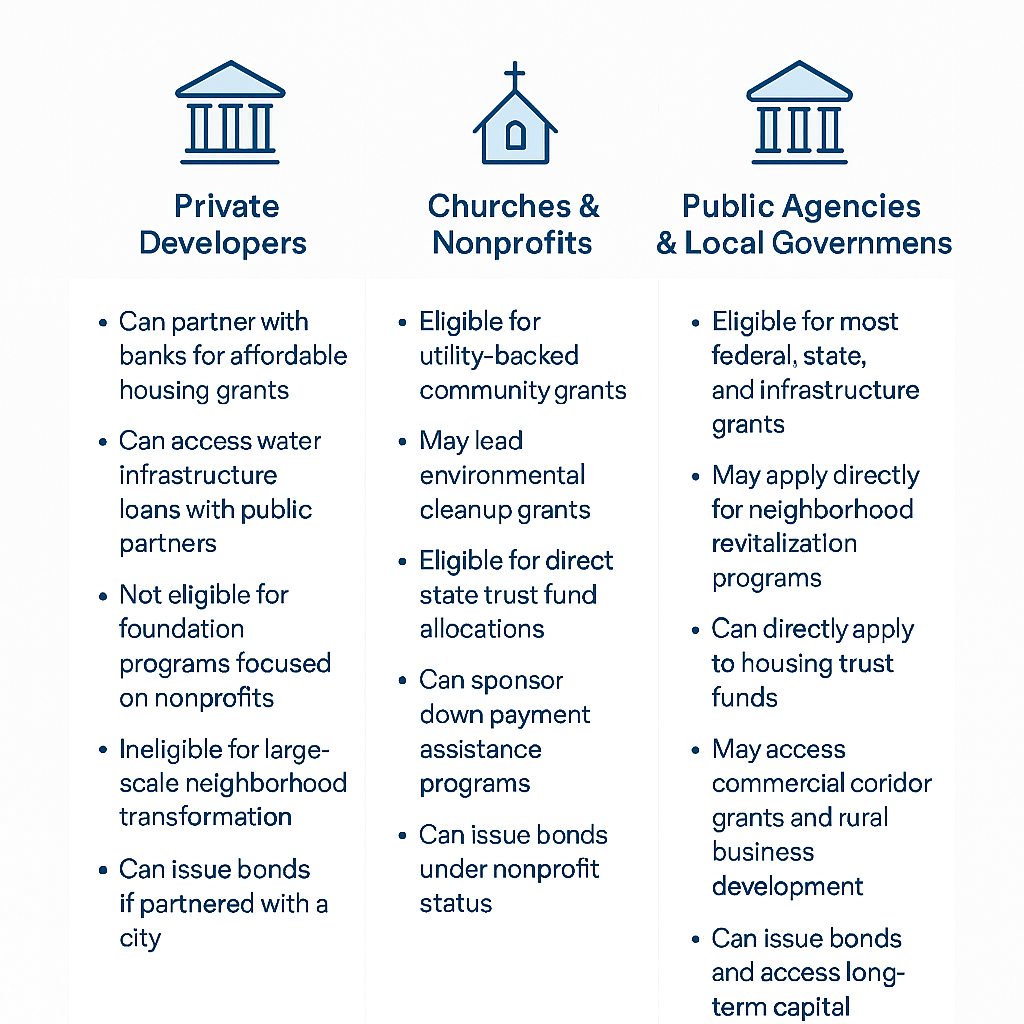

Private Developer: Build and Sell

- Homes are built and sold to qualified buyers

- Bond proceeds are received upfront at closing

- Construction loan is paid off immediately upon sale

- Mortgage rates are lower than market levels

- Ideal for buyers with moderate incomes and first-time status

Church or Nonprofit: Build, Sell, Retire Bond

- Organization serves as sponsor of bond issuance

- No state volume-cap needed if properly structured

- Construction is completed and homes are sold at affordable prices

- All bond obligations are cleared upon sale—no ongoing compliance

- Optional buyer supports may include down payment assistance or lease-to-own pathways

Steps to Implement

- Engage your state housing finance agency for bond approval

- Select a lending partner experienced in public-purpose financing

- Identify land parcels where moderate-income households can qualify

- Establish fair pricing model and buyer intake process

- Build 10–20 homes as an initial pilot to prove out process

How the Bonds Work

The primary tool for financing these homes is called a Mortgage Revenue Bond. These are special-purpose bonds issued by a public entity—usually a state or local housing finance agency—to help fund affordable homeownership. The technical name is "Single-Family Mortgage Revenue Bonds" and they are federally authorized under Section 143 of the Internal Revenue Code.

Bond proceeds are used to buy mortgages or support home loans for qualified buyers. Instead of the developer or sponsor taking out expensive private loans, the public agency raises funds through the bond sale. The money is then used to finance mortgages at below-market interest rates. Buyers repay the mortgage, and those payments are used to repay bondholders.

Most states have a designated authority that issues these bonds—such as the Alabama Housing Finance Authority. For nonprofit sponsors, these bonds may not count against the state's "volume cap," meaning they can be issued more easily without competing for limited federal allocations.

Key Terms

- Mortgage Revenue Bond (MRB): A bond issued by a government entity to support below-market mortgage lending for income-qualified buyers.

- Volume Cap: The federally limited annual amount of tax-exempt bonds a state can issue. Nonprofits may qualify for exemption.

- Bond Issuer: Typically a state housing finance agency authorized to sell bonds and manage repayment.

- Bond Proceeds: The funds raised from the public sale of bonds, used to finance mortgages or pay for housing construction.

These bonds are widely accepted in the investment market and have enabled homeownership for millions of families nationwide. According to the Council of Development Finance Agencies, over 3.5 million households have benefited from MRBs since the program's creation.

Reference: Internal Revenue Code §143, CDFA MRB Resource Center – www.cdfa.net

Multifamily Rental Finance Options

Three practical structures—each matched to a different sponsor profile—keep ownership local and financing costs low.

Model 1 • Nonprofit Bonds

- No volume cap: Issue anytime, skip state queues

- Mission alignment: Own 100 % of the project

- Simple compliance: Avoid tax-credit red tape

- Affordability: 75 % ≤ 80 % AMI; 20 % ≤ 50 % AMI

Model 2 • Developer Bonds + GSE

- Fast execution: Fannie Mae DUS / Freddie Mac Optigo

- No insurance fees: GSE credit enhancement

- Workforce focus: 80 %–120 % AMI rents

- Scalable: Replicate across markets

Model 3 • 80/20 Standby Equity

- Last resort: Use only when other credit unavailable

- Costly capital: 8–12 % preferred return

- No carve-outs: Equity absorbs first losses

- Flexible exit: Buy out partner after stabilization

Cost Check • $15 M Project | 5-Year Exit

| Metric | Standby Equity | Bond Insurance |

|---|---|---|

| Annual cost (mid) | $300 K | $75 K |

| 5-year total | $1.5 M | $375 K |

Preferred equity is roughly 4× the cost of bond insurance over a five-year hold.

Choose Your Risk Cover

- Basic bond insurance: Cheapest; PHA recourse up to 30–50 % on carve-outs

- Equity overlay (10 %): Adds buffer for environmental / force-majeure gaps

- Full equity partner (20 %): Broadest protection; highest cost of capital

Commercial Development Grants & Finance Models

Secure federal grants and financing to create sustainable economic ecosystems within workforce‑housing communities that provide additional revenue streams and essential services for residents.

🚨 Active Grant Opportunities – August 2025

Multiple federal programs are currently accepting applications.

Deadlines vary – contact North Star Group for assistance.

Available Grants

▼HUD Choice Neighborhoods

Up to $50M | $500K PlanningTransforms distressed housing into mixed‑income communities with commercial components.

- Commercial kitchen facilities

- Mixed‑use retail spaces

- Community health centers

- Business incubators

EDA Public Works Program

Rolling applicationsFunds infrastructure that supports commercial development in distressed communities.

- Business incubators

- Workforce‑training facilities

- Multi‑tenant commercial buildings

- Infrastructure improvements

USDA Rural Business Development

No max | Priority smaller requestsSupports rural commercial‑development projects including incubators and community facilities.

- Business incubators

- Technical‑assistance programs

- Market research & feasibility studies

- Rural business‑training centers

USDA Rural Community Development

$5 M FY 2025Technical assistance & financial support for housing and community development.

- Community facilities

- Economic‑development projects

- Technical assistance

- Capacity building

HUD Community Development Block Grant

Annual formula fundingFlexible funding for community & commercial facilities in low‑income areas.

- Public‑facility construction

- Business‑development assistance

- Economic‑development projects

- Community centers

GA Rural Workforce Housing Initiative

$28 M FY 2025 | $6 M FY 2026State‑specific program for infrastructure linked to workforce‑housing developments.

- Senior housing

- Commercial development

- Infrastructure improvements

- Mixed‑use developments

Financing Models

▼New Markets Tax Credit Low‑income areas

Credit Structure

- Long‑term, fixed‑rate financing

- Covers 40 % of project costs

- Below‑market interest rates

- Creates local jobs

- 39 % tax credit over 7 years

- Attracts private investment

- Can finance up to 100 % of costs

- Flexible terms for community projects

Eligible Projects

- Commercial real estate in qualified areas

- Community & healthcare facilities

- Educational & childcare centers

- Hospitality and boutique hotels

CDFI Comprehensive projects

Flexible Capital

- Patient capital with flexible terms

- Debt and equity options

- Mission‑aligned lenders

- Combines with other sources

Technical Assistance

- Business‑plan development

- Market analysis & feasibility

- Ongoing business coaching

- Network connections

SBA 504 Loan Program Local business dev.

Loan Features

- Up to $5 M per project (higher for energy/industrial)

- 10 % borrower equity (typical)

- Long‑term, fixed‑rate financing

- Equipment and real‑estate eligible

Benefits

- Preserves working capital

- Below‑market fixed rates

- Supports local job creation

- Pairable with other incentives

Smart Public Policy for the Automation Economy

Automation and artificial intelligence are accelerating rapidly across every industry. Without proactive policy intervention, millions of workers—particularly those over 40—face economic displacement and community decline. This section outlines a practical policy framework that transforms automation challenges into community wealth-building opportunities through federal grant funding and innovative public-private partnerships.

The Displacement Challenge We Face

Mid-Career Worker Struggles

Workers over 40 find it increasingly difficult to retrain for artificial intelligence-driven jobs. Traditional retraining programs show limited success, with many participants earning less even four years after completing programs.

Limited Political Solutions

Universal Basic Income proposals lack broad political support and sustainable funding mechanisms. Communities need practical alternatives that build long-term wealth rather than creating dependency.

Accelerating Wealth Concentration

Automation benefits primarily flow to technology company owners and shareholders, while displaced workers and their communities experience economic decline and reduced local investment.

Community Equity Model: A Practical Alternative

How the Model Works

- Community Partnership: Local governments and community development corporations partner with artificial intelligence and robotics companies seeking real-world testing environments.

- Equity Exchange: Companies receive access to test their automation technologies in live community settings, including municipal services, local businesses, and infrastructure projects.

- Community Ownership: In exchange for testing access and community support, companies provide small equity stakes (typically 3.5% to 5%) to community development funds.

- Long-term Wealth Building: As successful companies grow, community residents benefit through dividend payments and asset appreciation, creating sustainable income streams.

Why This Approach Succeeds

- Creates Ownership Rather Than Dependency: Communities gain actual stakes in automation success rather than temporary assistance payments.

- Provides Real-World Value: Companies benefit from authentic testing environments that laboratory settings cannot replicate.

- Spreads Risk Through Diversification: Community funds invest across multiple companies and technologies, reducing single-point-of-failure risks.

- Builds Local Capacity: Residents gain exposure to emerging technologies and develop relevant skills through direct participation.

Available Federal Grant Programs for Automation and Workforce Policy

Important Note: As of July 2025, many major federal grant competitions have concluded their current funding cycles. The programs below represent ongoing opportunities or upcoming funding rounds that communities can pursue for automation equity initiatives.

National Science Foundation Regional Innovation Engines (Future Rounds)

While the current round concluded with April 2025 deadlines, this $160 million program will likely announce future funding opportunities. Communities should prepare for upcoming competitions.

Potential Funding: Up to $160 million over 10 years per region in future rounds

Current Status: 29 semifinalists are being evaluated from the 2025 competition

Preparation Strategy: Develop regional coalitions and workforce development partnerships now to be ready for future announcements

Automation Relevance: Explicitly supports workforce development activities and human-technology partnerships

Economic Development Administration Technology Hubs (Limited Opportunities)

Current Tech Hub designations are complete, but EDA awaits additional Congressional appropriations to fund more hubs. Existing designees receive $500,000 accelerator awards.

Current Limitation: Only 5% of authorized $10 billion has been appropriated by Congress

Existing Awards: 31 designated hubs, with 18 receiving implementation grants

Future Possibility: Additional funding depends on Congressional appropriations

Alternative Strategy: Partner with existing designated hubs in your region

National Science Foundation Future of Work Research Program (Ongoing)

This program continues to accept proposals on an ongoing basis, making it one of the most accessible current opportunities for automation and workforce research.

Current Availability: Accepts proposals on rolling basis

Funding Levels: Medium grants up to $1 million, Large grants up to $2 million

Research Focus: Human-technology partnerships, workforce transitions, and future work design

Community Applications: Perfect for piloting community equity automation models

Department of Labor Workforce Programs (Check Current Status)

Department of Labor workforce programs operate on annual cycles. Round 6 of Workforce Opportunity for Rural Communities concluded, but other workforce programs may be available.

Recent Round: $49 million awarded in Round 6 (September 2024)

Action Required: Monitor Department of Labor Employment and Training Administration for new announcements

Alternative Programs: State Apprenticeship Expansion and other workforce development grants may be available

Geographic Focus: Rural and economically distressed communities

State and Local Economic Development Programs

While federal programs may be limited, many states operate their own economic development and workforce programs that could support automation equity initiatives.

Strategy: Contact your state economic development agency

Focus Areas: Workforce development, technology innovation, rural development

Local Partnerships: Community development corporations, workforce boards, regional planning organizations

Private Funding: Foundation grants and corporate social responsibility programs

Realistic Federal Grant Strategy for Community Equity Programs

Research and Development Phase

Apply for National Science Foundation Future of Work grants to study community equity models. This is the most accessible current opportunity for automation workforce research.

State and Regional Partnerships

While federal programs are limited, work with state economic development agencies and existing Technology Hub designees to develop pilot programs and build coalitions.

Monitor Future Opportunities

Stay connected with federal agencies for announcements of new funding cycles. Subscribe to grant notification services and maintain readiness for quick application turnaround.

Alternative Funding Sources

Pursue foundation grants, corporate partnerships, and state-level programs while building the research foundation needed for future federal competitions.

Why Federal Funding Supports Community Automation Policy

Aligns with Federal Priorities

Community equity automation programs address workforce development, technology innovation, and regional economic development—all current federal funding priorities.

Demonstrates Measurable Impact

Grant programs require specific metrics for job creation, workforce development, and economic growth that community equity models can readily provide.

Builds Sustainable Infrastructure

Unlike temporary assistance programs, equity-based approaches create permanent community assets that continue generating benefits beyond grant periods.

Reduces Government Burden

Private sector equity contributions reduce long-term public funding requirements while maintaining community benefits and workforce development outcomes.

Emerging Financial Innovations

The workforce housing sector is rapidly evolving with new financing mechanisms that leverage technology and innovative partnerships:

Crowdfunding Platforms

Regulation Crowdfunding allows anyone to invest in real estate projects, with platforms like Small Change specifically targeting community-impact housing developments.

Blockchain and Digital Assets

Emerging technologies that create new investment vehicles and reduce transaction costs through smart contracts and tokenized real estate ownership.

Impact Investment Funds

Private capital specifically targeting measurable social and environmental outcomes alongside financial returns in the housing sector.

Green Building Incentives

Specialized financing for energy-efficient construction including carbon credit integration and climate resilience bonds for adaptive housing design.

Additional Financing Tools

Specialized tools beyond grants and bonds.

Tax Increment Financing

Municipalities capture increased property tax revenue from new development to finance infrastructure and housing projects. Particularly useful for mixed-use developments where housing creates broader economic benefits.

Opportunity Zones

Federal tax incentives encourage long-term private investment in designated low-income census tracts. Can provide significant capital gains deferrals and reductions for workforce housing projects.

Community Land Trusts

Nonprofit organizations hold land in perpetual trust while residents own buildings. Keeps housing affordable across generations while allowing homeowners to build equity.

Low-Income Housing Tax Credits

The largest source of affordable rental housing financing in the United States. While complex, these credits can be combined with other financing for deeper affordability.

New Markets Tax Credits

Federal tax credit program that encourages investment in low-income communities. Especially valuable for mixed-use developments combining housing with commercial or community facilities.

Shared Equity Programs

Various models where public or nonprofit partners retain partial ownership to maintain affordability. Includes shared appreciation mortgages and deed-restricted homeownership.

Employer-Assisted Housing

Partnerships with major employers like hospitals, universities, and manufacturers to provide down payment assistance, forgivable loans, or direct development funding for workforce housing.

Social Impact Bonds

Pay-for-success financing where private investors fund programs and receive returns based on measurable social outcomes. Emerging tool for housing programs with clear performance metrics.

Real Estate Crowdfunding

Online platforms that allow multiple investors to pool small amounts of money to fund affordable housing projects. Some platforms like Small Change focus specifically on community-impact developments with minimums as low as $10.

Federal Home Loan Bank Programs

Each Federal Home Loan Bank must contribute 10% of earnings to affordable housing through competitive and homeownership programs. Provides grants up to $1.25 million per project through member financial institutions.

Appraisal Gap Financing

Grants or subsidies that cover the difference between appraised value and market value in disinvested communities. Helps facilitate rehabilitation and homeownership where traditional financing falls short.

Performance-Based Contracting

Agreements where payments are tied to specific housing outcomes and measurable community benefits. Aligns developer incentives with long-term community goals and housing performance metrics.

Community Bonds

Local investment tools that transform nonprofit social capital into financial capital. Allow community members to directly invest in local housing projects with competitive returns and social impact.

More Grant Programs

Additional federal and state funding sources:

USDA Rural Development Programs

Multiple specialized housing programs including direct loans, guaranteed rental housing, and preservation grants for rural workforce housing.

Community Development Block Grants

Flexible HUD funding that local governments can use for housing development, infrastructure, and community facilities supporting workforce housing.

HOME Investment Partnerships

Federal block grant program providing states and localities with funding for affordable housing activities including new construction and rehabilitation.

State Housing Trust Funds

Most states operate dedicated housing trust funds with ongoing funding cycles for affordable housing development and preservation.

Federal Home Loan Bank Affordable Housing Program

Competitive grants and homeownership set-aside programs funded by Federal Home Loan Bank earnings. Available through member financial institutions nationwide.

Environmental Protection Agency Brownfields

Assessment and cleanup grants for contaminated properties that can be redeveloped for workforce housing. Particularly valuable for urban infill projects.

Choice Neighborhoods Implementation

Competitive grants up to $50 million for comprehensive neighborhood transformation including housing replacement and community development in distressed areas.

Advanced Implementation Strategies

Sophisticated approaches:

Public Housing Authority Development Pathways

Public Housing Authorities may have certain advantages for affordable housing development through project-based vouchers and municipal bond financing. These pathways illustrate potential approaches that integrate innovative development models with public-private partnerships, though each situation requires careful evaluation of local conditions and regulatory requirements.

Development Model Considerations

Wellness-Focused Design Approach

Certain development models incorporate wellness features in affordable housing. These approaches require careful cost-benefit analysis to determine their appropriateness for specific projects and communities.

Potential PHA Advantages for Affordable Housing

Innovative Development Approaches

Development models like Serenity Village may offer wellness features that could create differentiated housing, though implementation would require careful cost-benefit analysis.

Project-Based Voucher Potential

Federal rent payments for project-based vouchers may provide stable revenue streams that could support municipal bond debt service, subject to HUD regulations and local housing authority capacity.

Possible Bond Authority

Housing authorities may have access to tax-exempt bond financing that could offer lower interest rates than private developers, though bond capacity and credit ratings vary by jurisdiction.

Grant Program Alignment

Housing authority projects may align well with federal grant programs, though competition for funding is intense and success depends on many local factors.

Established Relationships

Existing connections with HUD, state agencies, and local partners streamline approval processes and reduce development timeline risks.

Illustrative 5-Phase Development Process

The following phases represent one possible approach to affordable housing development. Actual timelines, funding availability, and regulatory requirements vary significantly by location and would require thorough feasibility analysis before proceeding.

Foundation Building

Explore partnership frameworks and potential planning funding sources to assess development feasibility.

Comprehensive Planning

If initial feasibility appears positive, conduct comprehensive analysis using available grant funding or other resources.

Financing Assembly

If feasibility studies support proceeding, explore permanent financing options that may include municipal bond issuance.

Construction & Development

Execute construction while preparing for lease-up with guaranteed project-based voucher tenants.

Operations & Expansion

Achieve stabilized operations and leverage success for additional workforce housing development.

Alternative Pathway: Church-Sponsored Development

Churches and faith-based organizations may also explore similar development approaches, though with different structures and considerations. These pathways are illustrative and would require careful evaluation of local conditions, regulations, and organizational capacity.

Potential Church Advantages

Possible Development Structures

Churches considering housing development might explore various approaches, each with distinct legal, financial, and operational implications:

Key Considerations for Churches

Important Success Considerations

Affordable housing development involves numerous complex factors that require careful evaluation. Success depends on many variables that are specific to local conditions and organizational capacity.

Development Approach Assessment

Construction methods and design features require thorough cost-benefit analysis to ensure they provide practical value within available budgets and maintenance capabilities.

Partnership Structure Clarity

Public-private partnerships require clearly defined roles, responsibilities, and risk allocation, with appropriate legal and financial protections for all parties.

Voucher Program Capacity

Project-based voucher commitments must align with Housing Authority capacity, HUD regulations, and long-term operational capabilities.

Community and Market Conditions

Local market conditions, community support, and regulatory environment significantly impact project feasibility and should be thoroughly assessed.

Financial Sustainability Planning

Conservative financial projections, appropriate contingency planning, and realistic debt coverage assumptions are essential for long-term project success.

Municipal Bond Financing Considerations

Project-based vouchers may provide stable revenue streams that could support investment grade bond ratings in some circumstances, though outcomes depend on numerous factors including:

Ready to Get Started?

Custom-scoped engagements based on your timeline and funding goals.

Schedule Discovery Call